Cyber Risk Management that actually reduces your risk

Take control of cyber risk with the only solution that translates cybersecurity controls into actionable financial prioritization, and backstops cyber losses with top-rated cyber insurance.

OUR APPROACH

Organizations must solve for cyber as both a technical and financial risk

Only Resilience brings together your security posture, real-time threats, and actual claims data—with cyber insurance—to tell you exactly which security actions will reduce your biggest financial risks.

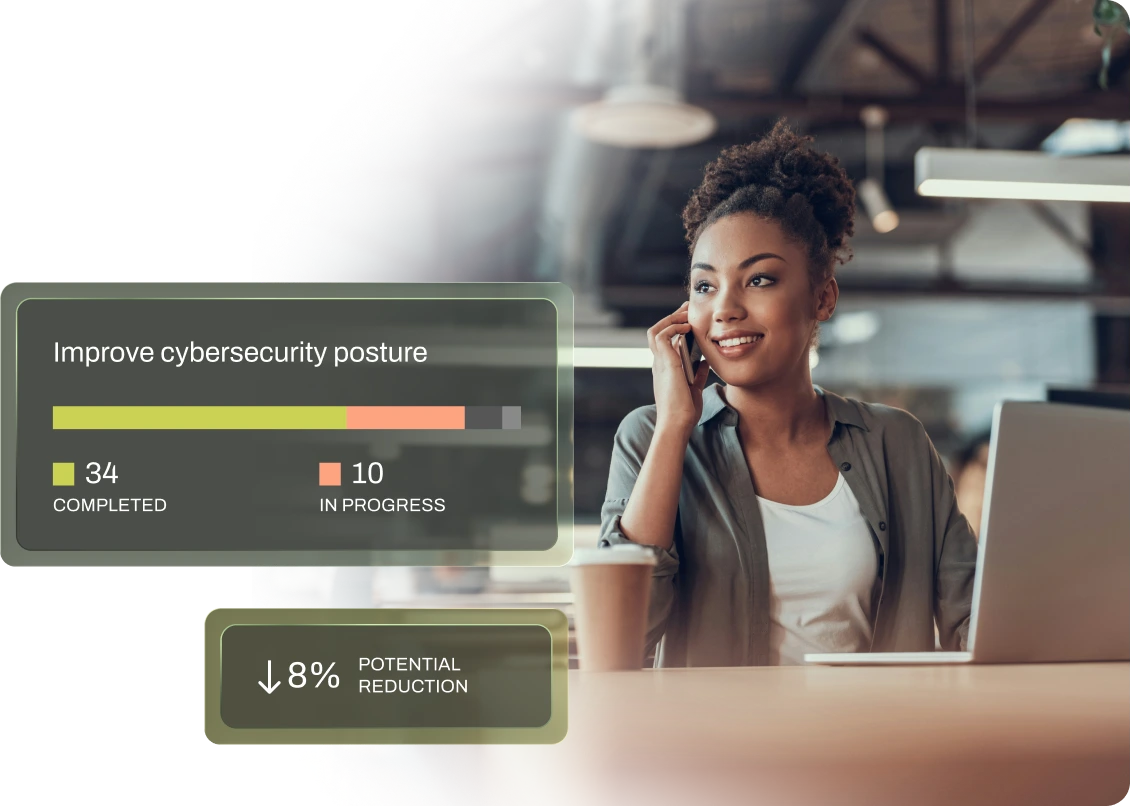

Track: Enterprise Risk Visibility

Track vendor, business, and operational risks across all your business units and subsidiaries.

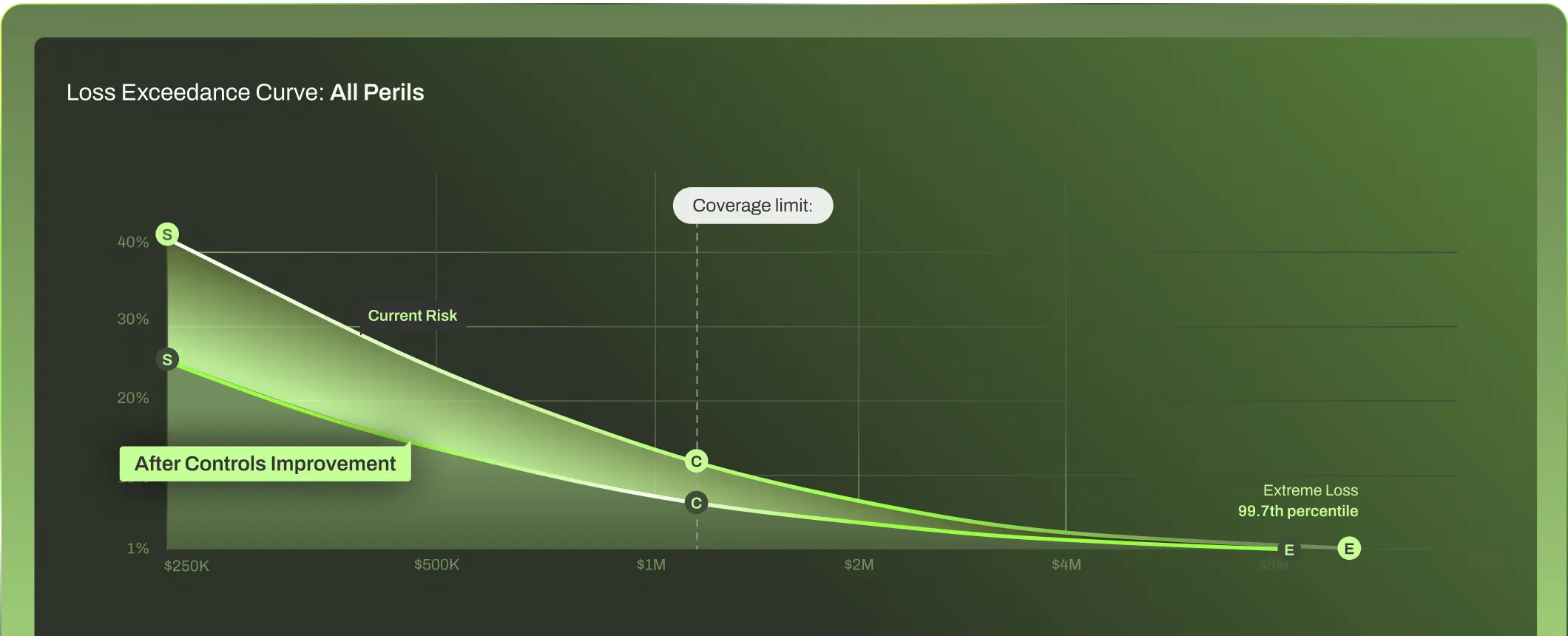

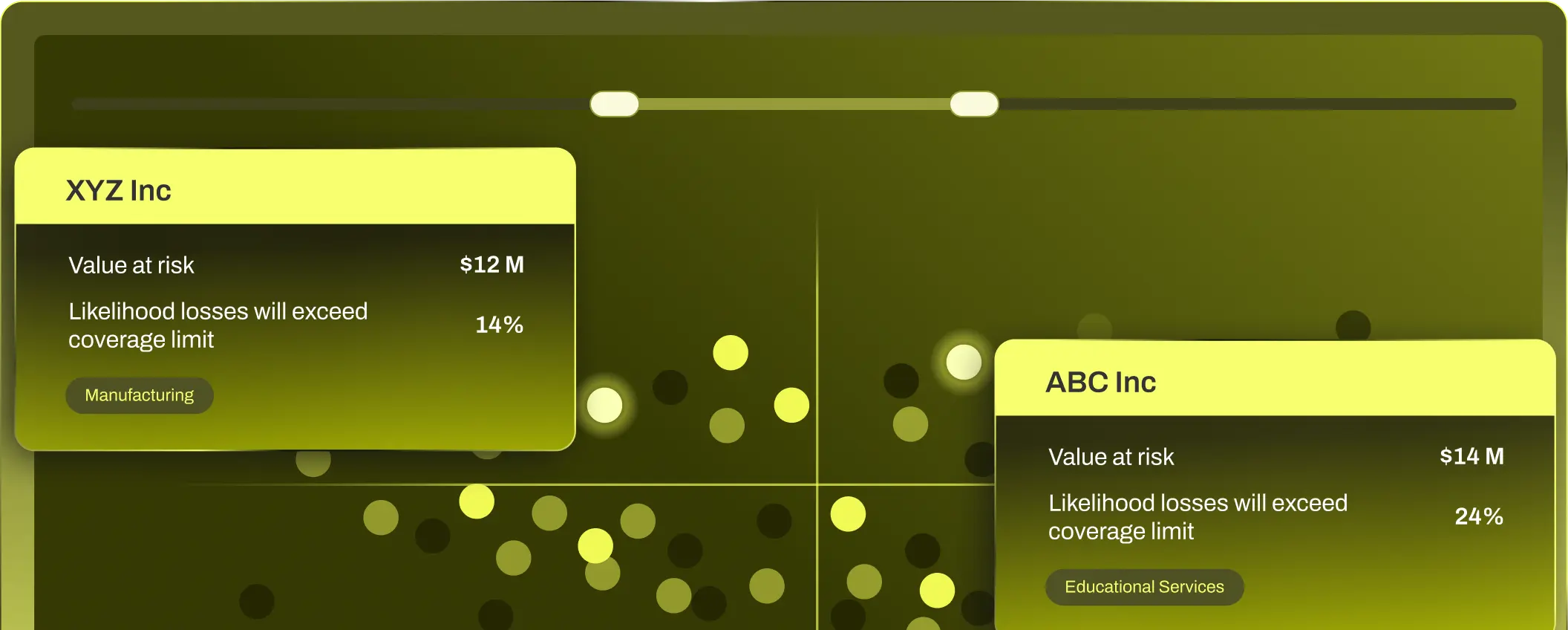

Translate: Risk Quantification

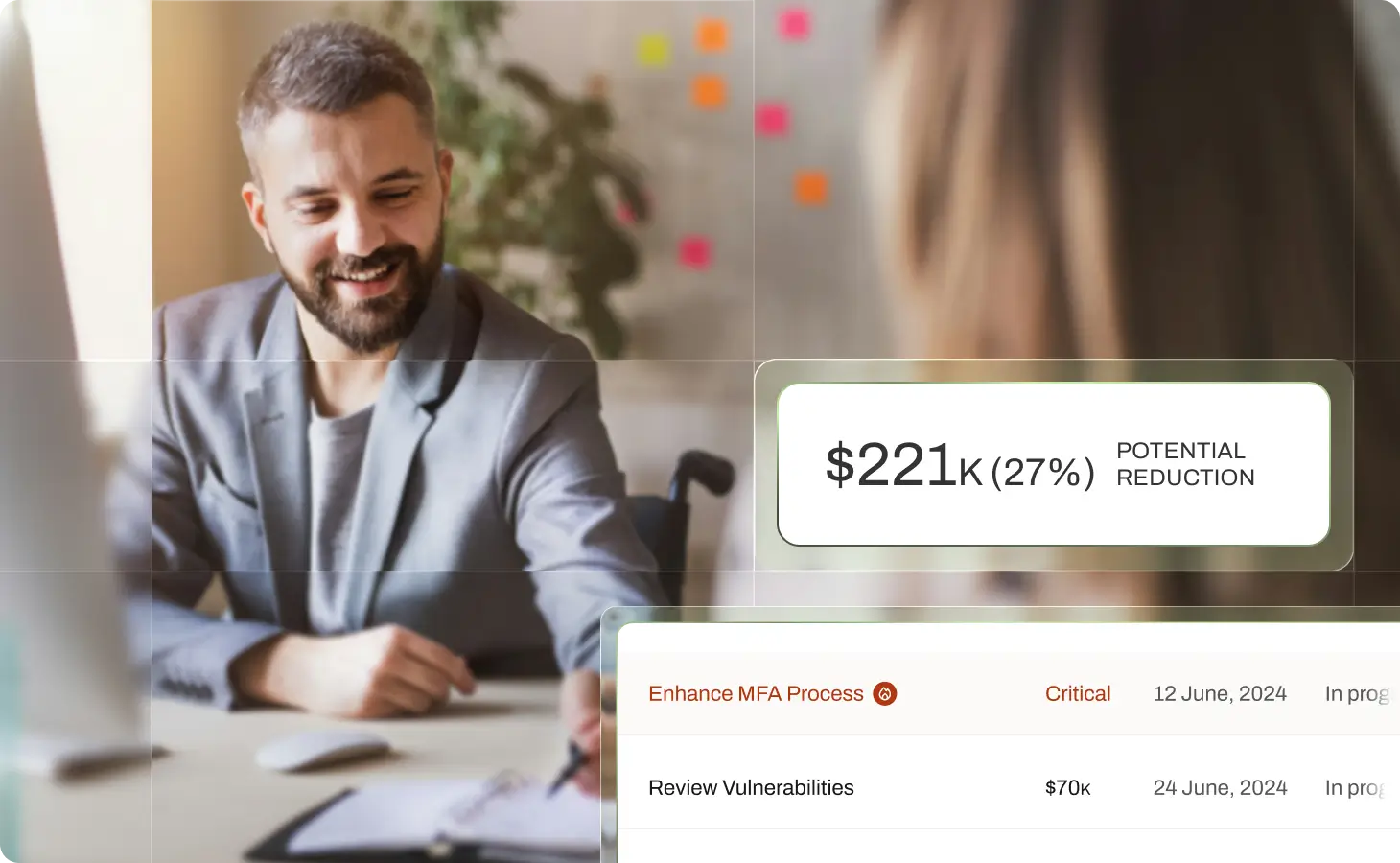

Translate your company’s technical security posture into financial impact with AI-powered risk quantification models.

Transfer: Cyber Insurance

Transfer cyber risk with top-rated cyber insurance and tools that actually help prevent losses in the first place.

Stakeholder Alignment

Bridge the gap between

risk, security, and finance leadership

CISO

Make cybersecurity a business enabler

Show executives the dollar value of your security investments—with proof they actually work.

CFO

Protect the treasury and reduce risk

Show how cyber risks impact your bottom line, predict potential losses, and prove your security budget is worth it.

RISK MANAGER

Transfer risk through cyber insurance

Lower your cyber risk with the solution that actually prevents losses.

CYBER RISK MANAGEMENT

Everything you need to measure and manage your cyber risk

Get comprehensive cyber insurance for when you need it, plus tools to prevent losses in the first place.

Top-rated coverage with broad market appetite

Experienced, sustainable underwriting

24/7 in-house claims and incident management

Prioritize the risks that matter most to your business—quantified using real claims data and validated by security experts.

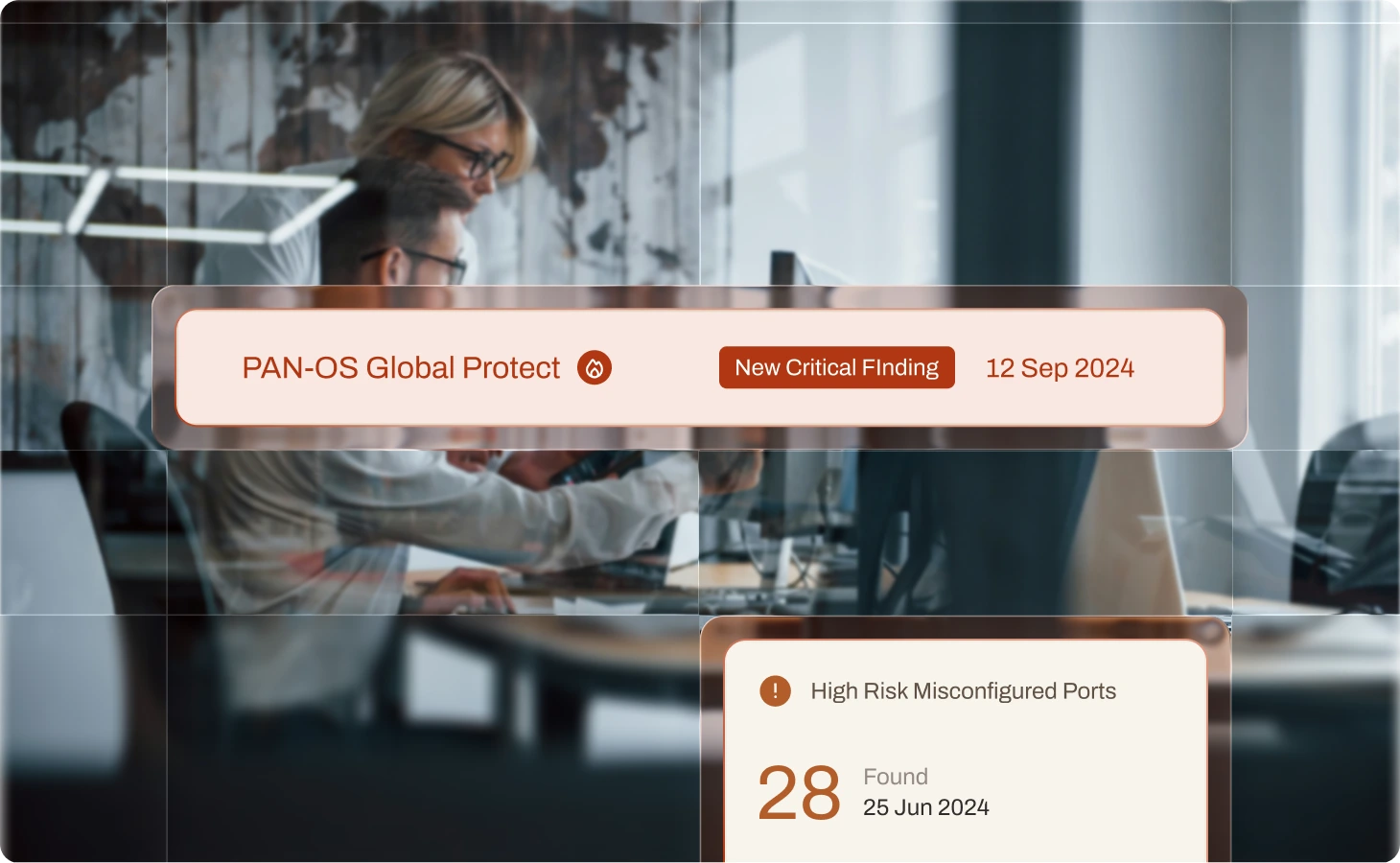

Real-time risk monitoring and mitigation

Financially quantified controls prioritization

Real-world attack scenario testing and validation

Get ongoing, dollar-based risk assessments for your entire organization—completely automated.

Automated risk assessments for every subsidiary and business unit

See which security controls matter most—ranked by dollar impact

Monitor threats across your entire organization from one place

![]()

WHY RESILIENCE?

See what the Resilience Solution has to offer

Make data-backed, informed decisions

CYBER ACTION PLAN

Stop wasting budget on controls that don’t actually work. We help you manage cyber risk the same way we underwrite it—by analyzing proven claims data to create clear, dollar-based action plans.

Justify and prove the value of your security program

CYBER RISK QUANTIFICATION

Know which vulnerabilities can drive material loss

RISK OPERATIONS CENTER

Create ongoing visibility into your entire portfolio

MULTI-ENTITY & PORTFOLIO RISK

BROAD MARKET APPETITE

A global partner you can count on

Available Coverage

Cyber Insurance, Tech E&O

Industries Covered

Healthcare, Higher Education, Financial Institutions & Financial Services, Manufacturing, Construction, Law Firms, Professional Services, Public Entities, Retail, Hospitality, Technology, Life Sciences, Medical Devices, Pharmaceuticals

Available Coverage

Cyber Insurance, Tech E&O

Industries Covered

Healthcare, Higher Education, Financial Institutions & Financial Services, Manufacturing, Construction, Law Firms, Professional Services, Public Entities, Retail, Hospitality, Technology, Life Sciences, Medical Devices, Pharmaceuticals

Available Coverage

Cyber Insurance, Tech E&O

Industries Covered

Healthcare, Higher Education, Financial Institutions & Financial Services, Manufacturing, Construction, Law Firms, Professional Services, Public Entities

Available Coverage

Cyber Insurance, Tech E&O

Industries Covered

Healthcare, Higher Education, Financial Institutions & Financial Services, Manufacturing, Construction, Law Firms, Professional Services, Public Entities, Retail, Hospitality, Technology, Life Sciences, Medical Devices, Pharmaceuticals

Available Coverage

Cyber Insurance, Tech E&O

Industries Covered

Healthcare, Higher Education, Financial Institutions & Financial Services, Manufacturing, Construction, Law Firms, Professional Services, Public Entities, Retail, Hospitality, Technology, Life Sciences, Medical Devices, Pharmaceuticals

Available Coverage

Cyber Insurance, Tech E&O

Industries Covered

Healthcare, Higher Education, Financial Institutions & Financial Services, Manufacturing, Construction, Law Firms, Professional Services, Public Entities, Retail, Hospitality, Technology, Life Sciences, Medical Devices, Pharmaceuticals

Available Coverage

Cyber Insurance, Tech E&O

Industries Covered

Healthcare, Higher Education, Financial Institutions & Financial Services, Manufacturing, Construction, Law Firms, Professional Services, Public Entities, Retail, Hospitality, Technology, Life Sciences, Medical Devices, Pharmaceuticals

Available Coverage

Cyber Insurance, Tech E&O

Industries Covered

Healthcare, Higher Education, Financial Institutions & Financial Services, Manufacturing, Construction, Law Firms, Professional Services, Public Entities, Retail, Hospitality, Technology, Life Sciences, Medical Devices, Pharmaceuticals

Available Coverage

Cyber Insurance, Tech E&O

Industries Covered

Healthcare, Higher Education, Financial Institutions & Financial Services, Manufacturing, Construction, Law Firms, Professional Services, Public Entities, Retail, Hospitality, Technology, Life Sciences, Medical Devices, Pharmaceuticals

Available Coverage

Cyber Insurance, Tech E&O

Industries Covered

Healthcare, Higher Education, Financial Institutions & Financial Services, Manufacturing, Construction, Law Firms, Professional Services, Public Entities, Retail, Hospitality, Technology, Life Sciences, Medical Devices, Pharmaceuticals

REPORT

2026 Midyear Cyber Risk Report Shows the Impact of Cyber Resilience

Get the latest trends and analysis in cyber claims with our 2026 Midyear Cyber Risk Report and see how we’re helping organizations build Cyber Resilience.

CUSTOMER STORIES

See the business impact of

cyber resilience in action

RESOURCE CENTER

Stay ahead of cyber risk with the latest intel and insights

The time for

Resilience is now